3 June 2015

Westlake Chemical Corporation Presentation_

Deutsche Bank 6th Annual Global Industrials and

Basic Materials Conference

James Chao, Chairman of the Board Albert Chao, CEO

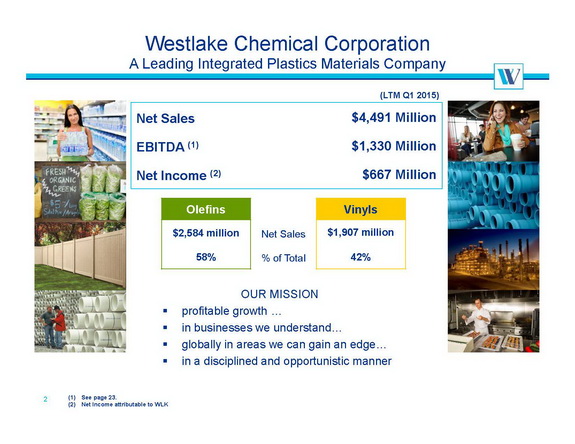

Westlake Chemical Net Income 2014 = USD 667 million

Westlake Chemical Net Sales 2014 = USD 4,491 million

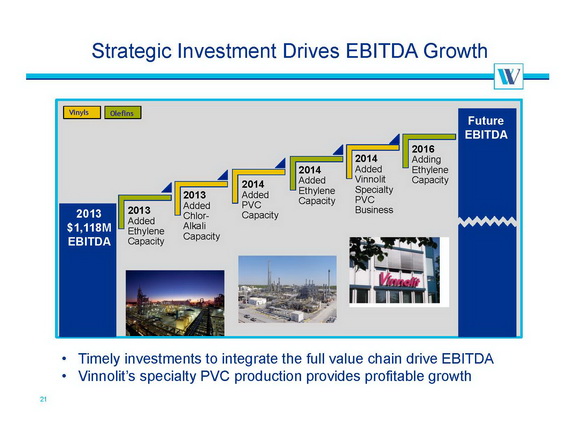

Westlake Chemical's Strategic Investment drives EBITDA growth

* Timely investments to integrate the full value chain drive EBITDA

* Vinnolit's specialty PVC production provides profitable growth

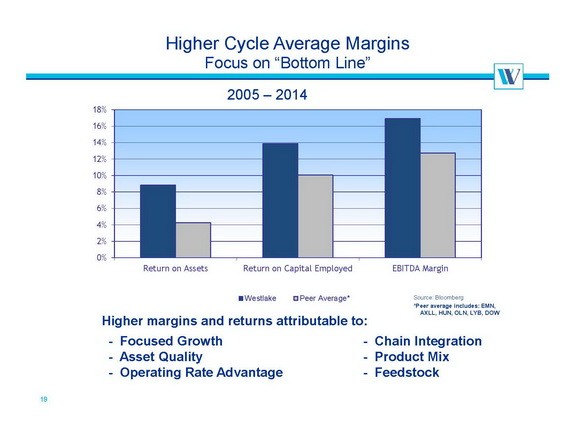

Higher Cycle Average Margins Focus on “Bottom Line”

Westlake Chemical higher margins and returns attributable to

* Focused growth

* Asset quality

* Operating rate advantage

* Chain integration

* Product mix

* Feedstock

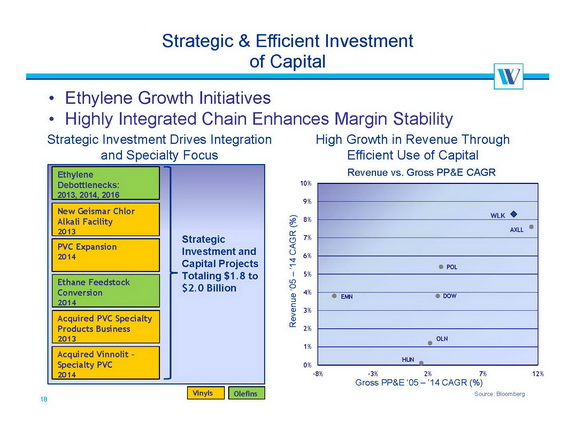

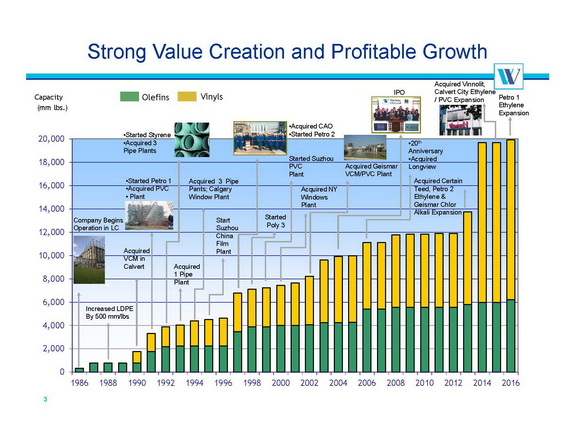

Westlake Chemical Strong value creation and profitable growth

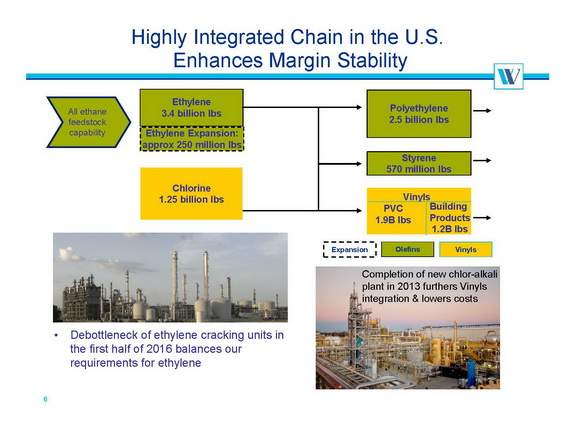

Highly integrated chain in the U.S. enhances margin stability

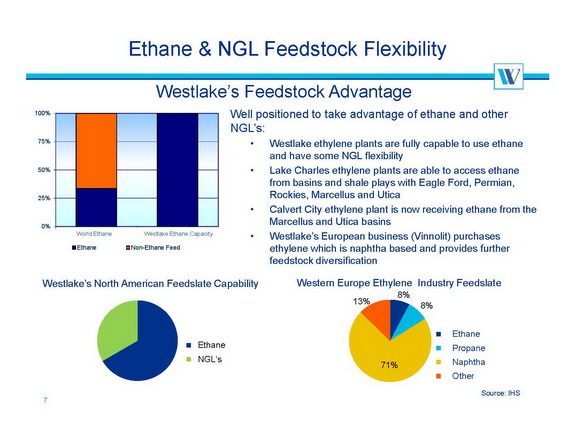

Westlake Chemical feedstock advantage

Ethane & NGL Feedstock flexibility

Well positioned to take advantage of ethane and other NGL’s:

• Westlake ethylene plants are fully capable to use ethane

and have some NGL flexibility

• Lake Charles ethylene plants are able to access ethane

from basins and shale plays with Eagle Ford, Permian,

Rockies, Marcellus and Utica

• Calvert City ethylene plant is now receiving ethane from the

Marcellus and Utica basins

• Westlake’s European business (Vinnolit) purchases

ethylene which is naphtha based and provides further

feedstock diversification

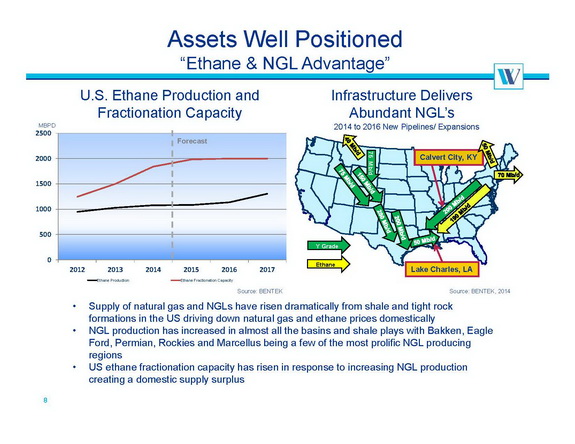

Assets Well Positioned “Ethane & NGL Advantage"

• Supply of natural gas and NGLs have risen dramatically

from shale and tight rock formations in the US

driving down natural gas and ethane prices domestically

• NGL production has increased in

almost all the basins and shale plays with Bakken,

EagleFord, Permian, Rockies and Marcellus

being a few of the most prolific NGL producing regions

• US ethane fractionation capacity has risen

in response to increasing NGL production

creating a domestic supply surplus

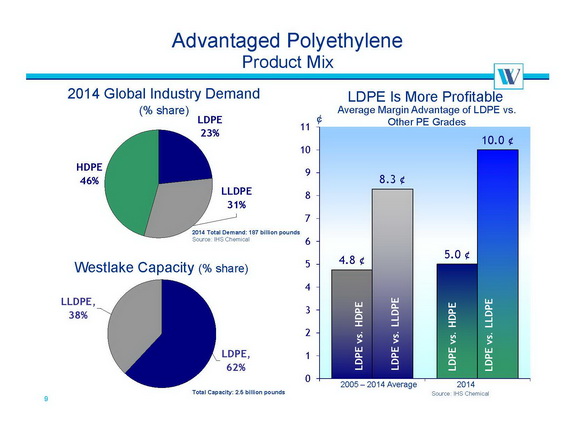

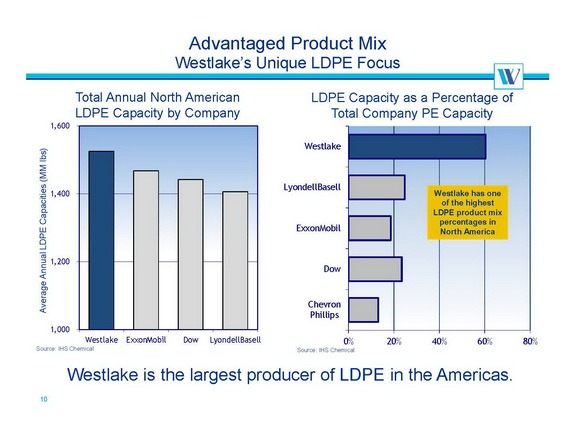

Advantaged Product Mix :

Westlake’s Unique LDPE Focus

LDPE Is More Profitable

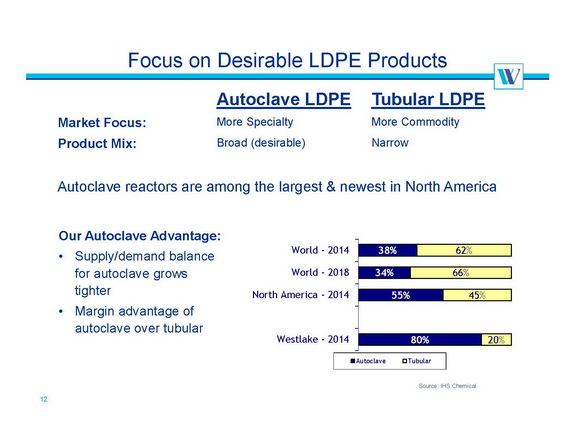

Focus on Desirable LDPE Products

Autoclave reactors are among the largest & newest in North America

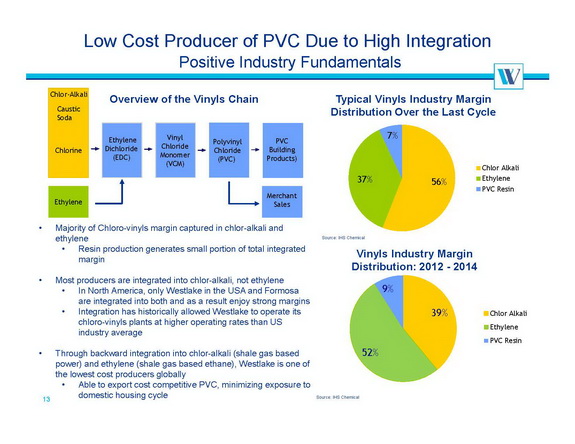

Low Cost Producer of PVC Due to High Integration

• Majority of Chloro-vinyls margin captured in chlor-alkali

and ethylene

• Resin production generates small portion of total integrated

margin

• Most producers are integrated into chlor-alkali, not ethylene

• In North America, only Westlake in the USA and Formosa

are integrated into both and as a result enjoy strong margins

• Integration has historically allowed Westlake to operate its

chloro-vinyls plants at higher operating rates than

US industry average

• Through backward integration into chlor-alkali

(shale gas based power) and ethylene (shale gas based ethane),

Westlake is one of the lowest cost producers globally

• Able to export cost competitive PVC, minimizing exposure to

domestic housing cycle

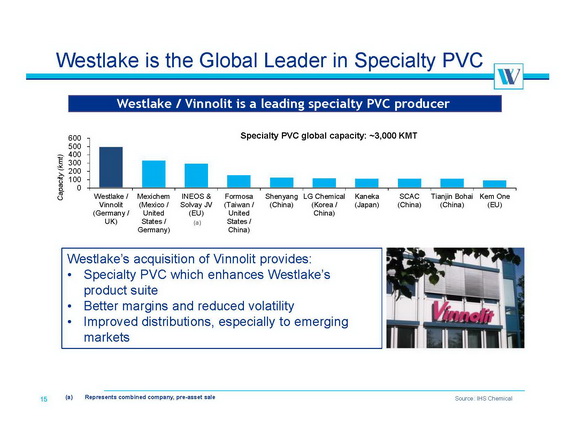

Westlake is the Global Leader in Specialty PVC

Westlake’s acquisition of Vinnolit provides:

• Specialty PVC which enhances Westlake’s product suite

• Better margins and reduced volatility

• Improved distributions, especially to emerging markets

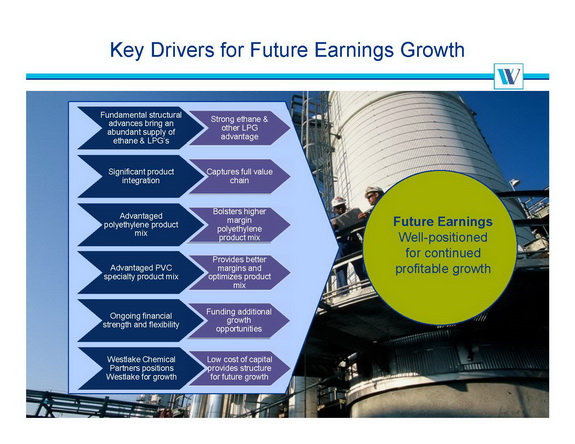

Westlake Chemical's key Drivers for Future Earnings Growth

VIEW FULL WESTLAKE PRESENATION

WWW.CHEMWINFO.COM BY KHUN PHICHAI